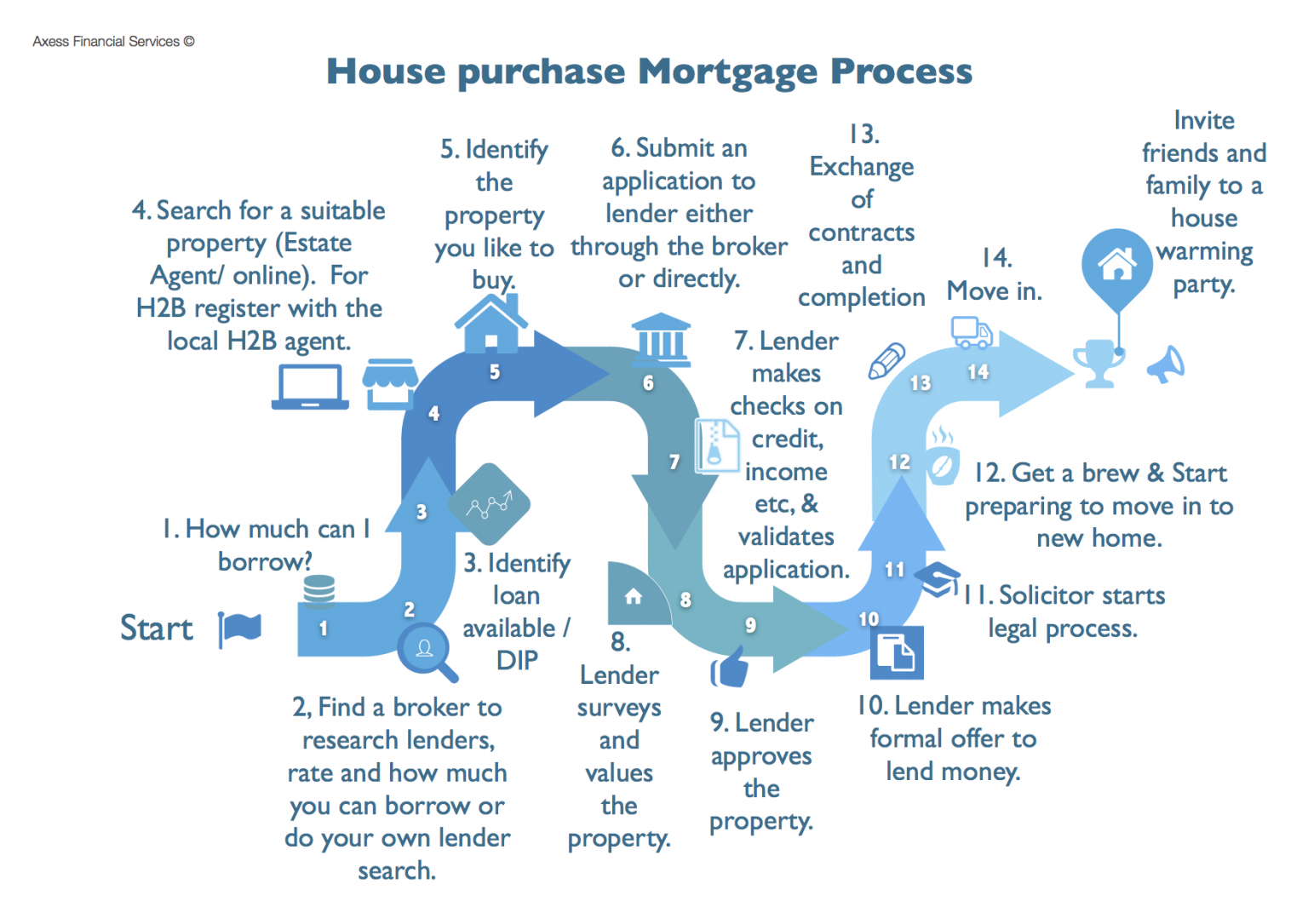

How much can I borrow?

Up to 4.5 -5x income in general and up to 5.5x for high income earners and professionals. It will depend on the following:

- Income

- Credit Score

- Credit & Loans

- Other fixed expenditure

- Number of Financial Dependents

Covid Alert

With the UK economy opening up and the chancellor Rishi Sunak’s new helping hand scheme for first-time buyers, have led many High Street lenders return to the 95% LTV mortgages. The extension of the stamp duty holiday to end of June has also helped.

- Physical valuation of property has restarted.

- Normal income multiples up to 85%. Reduce for higher.

- Self employed face additional restrictions.

- Lending to flats are limited by some lenders.

Which lender is the best?

When there are so many lenders in the market, how to choose the right one.

- It is not always the rate. A lower rate with higher fees not always best.

- Service standards.

- Will they lend to you based on your circumstances.

- Human underwriting.

Interest Rates.

First time buyer rates available from 1.21%.

Larger the deposit lower the rate. Many first time buyer deals come with FREE valuations and legals.

- Fixed rates to guarantee monthly payment.

- Discounted rates for lowest monthly payment

- Variable rates with no tie-in periods.

Affordability and maximum loan -how debt to income ratio and credit score affects income multiples.

Credit File for £2 – get credit file for £2 without monthly fees

Mortgages for LTD company Directors – how salary, dividends and net profit used in max loan.

On the Market – portal that allows agents to have greater control of propety listings.

Nestoria – aggregation from other property portals.

Nethouseprices – Past sale prices and estimated current values.

Prime Location – site run by zoopla.

PurpleBricks– online property portal with local agents.

Right move – largest property portal in UK.

Residential People – free to list portal.

SmartNewHomes – another site bought by zoopla, but dedicated to new builds only.

Tepilo – site set up by TV presenter Sarah Beeny selling for a fixed price. May not give an advantage of less competition as the site says same properties will be promoted through RightMove and Zoopla.

Zoopla – Portal from a large conglomerate that owns many financial sites – potential duplicates with other big sites.

HMRC Stamp duty calculator

Monthly Payment Calculator (downloadable excel format)

Standard First Time Buyer mortgage

- Maximum lending is 95%. Both with the new Helping hand scheme and outside of it.

- Standard FTB mortgage is a whole market mortgage for non-concessionary house purchases. Concessionary Shared ownership and Help to Buy Equity schemes also require 5% of the share purchased. So less deposit.

- Financial help for family in the form of a gifted deposit is acceptable.

- Available to those who had not owned a property in the past. Varies from lender to lender. Some lender will treat non-ownership in the past three years as a First Time Buyer.

- The rate is based on Loan to Value or LTV. Higher the percentage borrowed higher the rate. Special rates for FTBs.

- Can be up to 4 applicants and does not need to be all family members.

- Many lenders provide free surveys and legal service

Family Guarantor Mortgages

- Allows a First Time Buyer to borrow a higher loan than what standard income multiples would allow.

- Guarantors can be grandparents, parents, siblings and step relations.

- Several options available from providing a refundable deposit to having a charge over the guarantor’s property.

- Cannot own another property at the same time.

- Income multiples of up to 4.5x for the applicant.

- No adverse credit accepted.

Three main types

1. Family Deposit Account

Members of the family provides a security deposit (up to 20%) which is returned once the value of the property increases or sold. The deposit earns interest.

Lender provides 95% loan for purchase. Applicant provides 5% deposit.

2. Family Offset Account

Family holds up to 20% of deposit in an offset account on their own name. No interest is earned in the offset account.

Lender provides 95% of loan and applicant 5%. Interest is charged on 75% of the loan only, so gaining a saving on payments.

3. Family home as security

Lender takes a charge on parent’s / family member’s home and provide 100% loan for purchase.

Affordability based on applicant’s income. Applicant provides no deposit.

Example of a guarantor scheme: Family Offset Mortgage

Joint Borrower Sole Occupier

Is another type of family assisted mortgage. Where the surplus income of a parent/step parent can be used to boost the income multiples of the applicant. All secured (mortgage) and unsecured (credit) outgoing of the parent will be taken in to account for affordability.

- Only the occupier of the property will be named on the deeds. However, the parent/ family member will be party to the mortgage with joint and several liability for the debt. Some lenders will only allow close family members, e.g. parents, step-parents, siblings, while others will allow unconnected parties. All will be credit scored and credit assessed.

- As only one name on the deeds, there is no additional second home stamp duty charge for the supporter.

- Residential owner occupier mortgages only and up to 95% LTV. Loan can only be capital repayment basis.

- Affordability 4.5x to 5x joint income. Annualised outgoings for both applicants (e.g. mortgages, credit cards, loans, HP etc) will be deducted from income before applying multiples. The JBSO mortgage will be treated as an outgoing for the supporter for any credit assessment in the future.

- Minimum age 18. Maximum 2 applicants. No BTL property allowed.

- Both applicants must have taxable income, e.g. employed, self employed, pension.

- The supporter can be removed from the mortgage once the occupier’s income become sufficient to support the mortgage independently.

- Parent/ family members must take independent legal advice regarding their party to the debt.

Concessionary Lending for First Time Buyers

Help to Buy

Currently there is only one type of Help to Buy (H2B) scheme available, the Help to Buy Equity Loan Scheme, You require a deposit of at least 5%. The government then provides you with an Equity Loan of up to 20% in England excluding London, 40% in London and 15% in Scotland. Only available for new build home property. The government loan is interest free for the first 5 years. After 5 years you will have to pay the interest on the Equity Loan (except in Scotland).

The scheme is open both to first-time buyers and home movers purchasing a new-build property or remortgaging with a maximum purchase price of up to £600,000, from a registered developer.

The scheme is administered by Local HomeBuy Agents who assess and approve all applications.

New build property only – can be more expensive than pre-owned, have to rely on many intermediaries e.g. builder, help to buy adminisitrators, lender, selling agent.

Loose up to 20% future property price rises.

Cannot make any alterations to the property without permission from H2B scheme managers.

Sale price must acceptable to scheme provider (selling under value to family member etc not allowed).

Not available if there is adverse credit.

Help to Buy- Mortgage guarantee.

- You contribute: 5% of purchase price.

- Governmant provides you a loan: up to 20% of purchase price

- Mortgage Lender provides rest e.g. up to 75% outside London and 55% in London.

- Must use a registered Help to Buy agent (H2B) and the property needs to come from a H2B registered builder.

Pros

- Minimal deposit of only 5% to enter the property ladder.

- No interest payments in the first 5 years- so a very efficient way to borrow money.

- Low interest for a period after 5 years

- Option to pay off total loan (based on property value at time) at any time and own outright. Minimum repayment is 10% of market value.

Cons

- New build property is similar to buying a brand new car. You might like the idea of you are the first owner, but same as cars they are overpriced or has a new build premium. You are not likely to see any rise in value of the property in the next few years. It might even be worth less in the first 2 years. New build premium could be 10% – 20% of value.

- Rates are higher than for similar residential mortgages.

- Not available as guarantor mortgages, maximum lending is still limited to income earned. Lower income multiples than standard mortgages.

- Not all lenders lend to H2B so not all deals are available.

- Property cannot be let and you are not allowed to own any other property at same time.

- Not available if there is adverse credit i.e. over 3 month’s missed payment in the last 3 years, CCJs over £500 or bankruptcy within last three years.